This story was published and co-reported by Outlier Media and The Markup. WXYZ is a proud partner of Outlier Media. The Markup is a nonprofit, investigative newsroom that challenges technology to serve the public good.

The high cost of auto insurance pushed Clarissa Williams to move out of Detroit and all the way to California, where she thought it more likely she could get to work. She was right.

For Alana, the fact that she can’t afford to insure her car in Detroit has pushed her out of the job market altogether. She’s a retired preschool teacher, but she wants and needs to get back to work and back out into the world.

Tonya can’t afford car insurance in the city either, but she also can’t afford to not drive her son to school and herself to work, neither of which she can find in her neighborhood. She breaks the law every day by driving without insurance. She risks getting caught and racking up expensive fines she doesn’t know how she would pay.

The average cost of auto insurance in Detroit is $5,300 a year, more than any other big city in the country. A Detroiter making the city’s median income would spend one out of every seven of their dollars on auto insurance alone.

State reforms five years ago were supposed to bring relief. A 2019 law prohibited insurers from considering certain factors unrelated to driving, including ZIP codes, when setting rates.

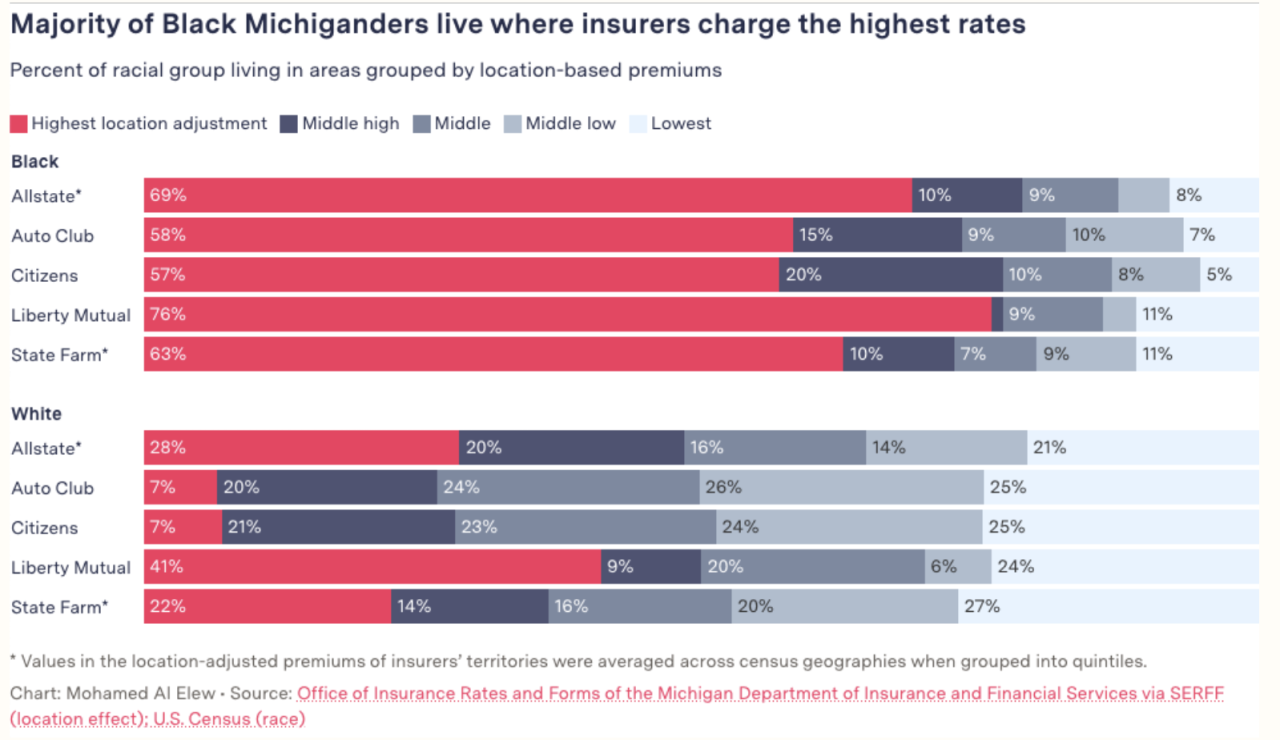

A new investigation from The Markup and Outlier Media shows how little the reforms did to stop insurers from using where people live to set their rates. These location adjustments are a burden on the majority of Black residents of the state, and much less so for white residents.

By cataloging how each insurer’s pricing algorithm takes location into account, we show how Michigan’s auto insurance reforms have failed to deliver on the promise of affordable insurance in Detroit. We found insurers are still using customers’ addresses as a proxy for risk in a way that charges higher premiums to customers in neighborhoods with more Black residents.

Most Detroiters already know living in the city means they pay more for their insurance, but insurers typically don’t allow individual shoppers to see how their rates would change at another address.

We worked with an insurance agent and three Detroit women to see how much location can impact rates on an individual level. We pulled quotes for premiums using their actual driving records and vehicles, but comparing their Detroit addresses with addresses just outside the city limits. Alana, Michelle, and Tonya are not these sources’ real names. Outlier and The Markup agreed to withhold their names because that practice is prohibited by the insurance agent’s employer and could be used to identify them.

Michelle’s quote for her Detroit address came in at $650 per month for full coverage, or 19% of her income — an astronomically high number by U.S. standards, but on par in Detroit. She figured a quote using her same driving record and vehicle would be lower outside the city.

The price landed like a gut punch anyway. If Michelle lived just across the city border in a neighborhood with a larger white population, she’d pay $414 per month for the same package, or 36% less. A little further from the city, in a much whiter and more well-off area, she’d pay $265 per month — less than half as much. For her part, Tonya could come close to affording bare-bones, liability only coverage in Detroit at just over $200 a month. But if she lived in the suburbs, she would only have to pay $110 a month.

How does location affect insurance rates?

Insurers start with a base rate to price individual policies, then adjust the policy cost depending on things like what kind of car somebody drives, how many accidents they’ve had and where they live. Location is just one of many factors insurers consider.

The investigation examined rates charged by the seven largest auto insurers in the state: Progressive, State Farm, Auto Club (which insures AAA members in Michigan), Auto-Owners, Allstate, Citizens and Liberty Mutual. These insurers used between a dozen and more than 70 different rating factors to arrive at a customer’s price. Allstate and Liberty Mutual used location to set their base rates; the rest used location to adjust their base rates.

Reporters at The Markup analyzed how each insurer’s algorithm weighted a customer’s address. They could then calculate how a driver’s rate is adjusted for Detroit and how it would change if they lived in Traverse City, for example. The effect can yield stark differences in rates, even when two places are actually very close to each other. These location effects also align closely with differences in racial demographics.

Is this only a problem in Detroit?

Detroit isn’t the only place with a high location multiplier, but the impact of living in Detroit on auto insurance rates is outsized.

Our investigation is based on what is known in civil rights law as a “disparate impact” analysis. We tested whether insurance companies took location into account in a way that could put a cost burden in predominantly Black areas, regardless of the intention behind those rates. Under the current regulatory system, these rates are all considered to be acceptable, legal practices.

The parts of Michigan where it is least expensive to buy auto insurance were, on average, 87% white. Even excluding Detroit, about half of the state’s Black population live in areas where insurers in our analysis use their highest location-related adjustments

The pricing structures of Auto Club and Citizens showed strong correlations between areas’ location multiplier and racial demographics. For both insurers, about 7% of the state’s white population lived in areas with the highest location multiplier, while more than half of Black Michiganders lived in those neighborhoods.

Citizens customers within neighborhoods in Benton Harbor, for example, would see a location multiplier nearly twice that for neighborhoods in St. Joseph. The two cities’ post offices are only three minutes away from each other. Benton Harbor is about 90% Black; St. Joseph, about 90% white.

For example, Auto Club customers in Detroit’s Cornerstone Village, a majority-Black neighborhood, faced a penalty of a location adjustment that was 50% higher than residents of Grosse Pointe Farms, an almost entirely white city right across Mack Avenue.

Sheila Cockrel, a lifelong Detroiter, former Detroit city councilmember, and current executive director of civic engagement nonprofit CitizenDetroit, tied the elevated rates paid by the state’s predominantly Black communities back to historic redlining practices that often trapped people of color in marginalized, segregated neighborhoods.

“They’re fundamentally connected, one flows from the other,” Cockrel said. “It’s not as blatant, but it’s still all rooted in the same set of expectations that the less white, the less middle-class the community is, the less value it has, and therefore the more risk there is in that neighborhood. And, therefore, you get to charge those people more money.”

The insurers whose pricing systems we analyzed defended the prices charged to policyholders across the state as reflecting the divergent costs associated with insuring drivers from one region to another.

Why didn’t reforms stop insurers from using location?

State lawmakers passed legislation in 2019 designed to lower costs across the state primarily through removing a requirement that all customers carry unlimited personal injury protection insurance to cover medical claims, and by putting in a cap on how much medical providers could charge for that care. Another element of the reforms, backed by many Detroit lawmakers and Mayor Mike Duggan, prohibited insurers from using “non-driving” factors like location and credit score to set insurance rates.

Michigan state Rep. Karen Whitsett, D-Detroit, said at the time in an op-ed, “Beginning July 2020, your driving record will be the primary factor determining your insurance rates.”

But the law only stopped insurance companies from using ZIP codes to set rates, not other location factors like census tract. In the aftermath of the reforms, the size of this loophole became more clear.

Before 2019, the price of car insurance in Michigan was the highest in the country, and it is now the sixth highest, using figures from The Zebra. The average cost of insurance in Detroit was more than $6,300 before reforms. It’s now on average $1,000 less a year, but is still the most expensive in the country when compared to other big cities. Mayor Duggan declined to comment on our findings.

“This report confirms what our residents have been telling us. Insurers are still finding ways to get around reforms intended to prevent discrimination,” said U.S. Rep. Rashida Tlaib, D-Detroit, who has introduced legislation that would take the cost of car insurance payments into account when calculating government benefits. “Ban zip codes and they come up with even more precise location discrimination,” she said.

Following the reforms, most insurers we examined shifted how they divided Michigan into geographic territories. Allstate and State Farm, which both previously used ZIP codes, divided the state into tiny geographic boxes, most of which were much smaller than a typical ZIP code area. Auto Club stopped using counties and shifted to an even smaller geographic unit called census tracts, which are areas drawn by the U.S. Census Bureau with an average population of 4,000. For example, Wayne County was divided into 611 tracts for the 2010 census. Citizens was the only insurer that used the same geography before and after the reform, but the company’s choice, called census block groups, are even smaller than census tracts. Liberty Mutual was the only insurer that switched to a larger geography, going from using ZIP codes to counties.

Auto-Owners and Progressive used ZIP codes before the reforms and moved to custom maps after. Because the maps were so customized, we could not match them accurately to census data, so we did not do a disparate impact analysis on these two insurance companies.

Regardless of how insurers defined their territories, the companies we analyzed still charged people living in Detroit more.

State Farm policyholders in a 97% Black portion of Detroit’s Morningside neighborhood saw a location adjustment nearly seven times that of Saline Township, about an hour’s drive southwest — the largest disparity in our analysis.

Are reasons like crime behind Detroit’s high insurance rates?

Insurers need enough money to cover claims, and state law requires them to consider things like population density, which can affect their losses and expenses, said Anita Fox, director of Michigan’s Department of Insurance and Financial Services, in an emailed statement.

State regulators are charged with deciding how closely location aligns with loss. Right now, they are accepting insurance companies’ assertions that the prices they charge to different locations are justified.

Eric Poe, CEO of CURE Auto Insurance, said shady towing fees and related legal costs in Detroit have cost his company millions, driving up rates for all customers in Detroit. (CURE is not one of the top seven insurers in Michigan, so it was not part of our analysis.)

Flynn Smith is a high school math teacher who lives in Detroit. He pays about $450 in auto insurance every month for his three older, fully paid-off cars. He carries only basic liability coverage, meaning insurance won’t cover most collisions, damage or theft.

“One of the ways I balance my budget is to take full coverage off my vehicles,” he said. “Why pay $4,000 a year for a car that is worth $4,000?”

Smith knows he’s being asked to pay more than people in the suburbs. “Somebody in Canton with the same car and same driving record should ideally be paying the same amount as I am. But I know that’s not happening,” he said.

“Is my car more likely to get stolen in the city of Detroit?” he asked. “I don’t think my minivan is on the top of anyone’s list.”

What did the insurers and state say about this investigation?

We reached out for comment to all seven of the insurance companies whose pricing systems we analyzed. The insurers, by and large, ignored our specific questions about rate-setting practices and defended the prices they charge policyholders across the state as reflecting the divergent costs associated with insuring drivers from one region to another.

“We believe our pricing accurately reflects the various risks associated with insuring vehicles in different parts of the state,” Auto Club spokesperson Adrienne Woodland wrote in a statement.

“We do not utilize, collect or consider information related to an individual’s race in underwriting, premium determination or claims settlement practices,” Liberty Mutual spokesperson Glenn Greenberg said in an email.

Representatives from Progressive and Citizens directed us to Nicole Mahrt-Ganley, an assistant vice president for public affairs at industry group American Property Casualty Insurance Association. “Unfair discrimination in insurance rating — meaning treating consumers with similar risk profiles differently — is uniformly prohibited by state law,” Mahrt-Ganley said. “There is a substantial amount of academic research indicating that insurers’ use of rating factors does not result in unfair discrimination.”

Laura Hall, a spokesperson for the state’s Department of Insurance and Financial Services, asserted that the disparate impact approach of our analysis was not broad enough to determine whether rates were fair.

The detailed responses from insurers and regulators, and more information on the methods we used, can be found in our methodology.

How can I save money on car insurance?

Most auto insurance customers renew their policies without much thought. But not David Palmer.

Every six months, Palmer (who is part of Outlier’s Detroit Documenters program) spends half a day seeking as many car insurance quotes as possible — while providing live social media commentary. The process is time-consuming and frustrating, but he believes it’s just part of the “annoyance tax” of living in Detroit and the only way to keep his costs down.

Most people don’t have time for all that work, and it wouldn’t be necessary if state lawmakers took meaningful action to reduce car insurance prices in Detroit.

Still, shopping around could make a real difference to your budget. Detroiters we spoke with had better luck getting lower rates when they were willing to switch insurance companies. Palmer says he’s had the most luck with Auto Club and Safeco, and the least with State Farm. But he’ll still check again in six months.

And ask for discounts. Make sure your insurer is giving you credit for all the discounts you are eligible for, like anti-theft devices, antilock brakes and student discounts. Because insurers change their policies frequently, ask for a rundown of all discounts available.